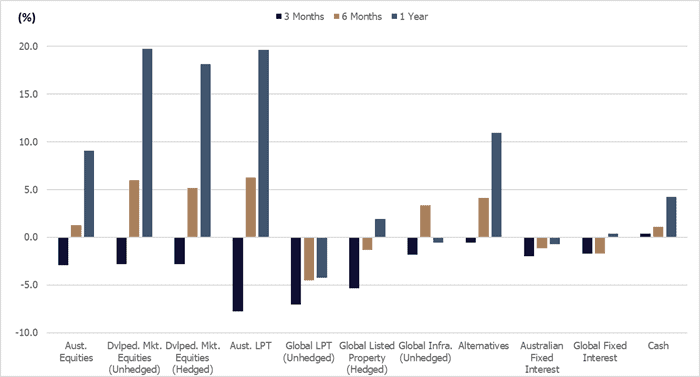

The equity market rally experienced over the March quarter stalled in April as investor sentiment moderated. Comparing forward pricing of interest rates in January vs. April 2024, we note there has been a material shift in expectations. Inflation which was on a downtrend has remained sticky around the 3%-4% mark.

Figure 1: Asset Class Performance as at 30 April 2024

Source: Allied Wealth, Morningstar.

Coming into 2024, portfolios retained a marginal underweight risk and an overweight in hedged international equities relative to unhedged.

The underweight in risk assets detracted from the return outcome over the March 2024 quarter as stock markets experienced a narrow market rally; this compared with the overweight to hedged international equities relative to unhedged which was broadly neutral over the assessment period.

Rally in risk assets was attributable to 2 key themes, equity earnings which have proven resilient over the last 2 quarters and have continued to pick up steam at the index level, and extremely positive risk-on sentiment contributed in part by expectations of interest rates falling. The latter theme has not played out as the market expected with stickier and higher inflation for longer leading to a market sell-off in April.

We note that this market environment is very unlike a lot of history and provide further discussion on the outlook in the sections below.

The economic and geopolitical rivalry between US, Europe and China has evolved into global trade protectionism with national security increasingly cited as a reason for trade tariffs and loose fiscal policy (government spending). Over the last quarter, we have seen US and Europe provide fiscal support (via tax breaks and funding assistance) to manufacturers of semiconductors, electric vehicles, and solar panels – with the intention of bolstering local manufacturing capabilities.

Moving forward, we expect to see more protectionist measures from both US and Europe (vs China); but how this will escalate remains too early to tell. The recently implemented tariffs on Chinese goods will incentivise the build-out of local factories over the next few years, reversing decades of trade globalisation.

As stewards of your capital, we remain primarily focused on the financial market implications for your portfolios. We expect this theme to be both supportive of economic growth and inflationary. On the equity side we expect this to translate into further earnings growth, but upside participation is skewed towards tech and defence sectors.

The build-out of local manufacturing capability represents additional capital expenditure which over the short-term basis will support economic growth; but the higher labour costs associated with the production of goods is expected to be passed through to the end consumer. Thus, we continue to expect inflation to be structurally higher over the medium to long term.

Overall while there are positive implications for corporate earnings; we remain concerned that the structurally higher inflation will also mean higher borrowing costs for businesses and consumers. In balancing the upside and downside considerations based on our investment outlook, we have decided to neutralise our underweight to risk assets.

Within international equities, we continue to maintain an overweight in hedged international equities relative to unhedged. The Australian Dollar (relative to US Dollar and Euros), at current valuations still look cheap relative to history.

| Asset Class | Portfolio Stance | Commentary |

| Domestic Equities | Neutral | We have maintained a Neutral portfolio stance in Australian equities. On a price-to-earnings basis, Australian equities look marginally overvalued relative to history, however the magnitude is not large enough to warrant a change in portfolio. |

| International Equities | Neutral | We have chosen to neutralise the underweight in International Equities; but within the asset class, we have selected to maintain the marginal overweight to hedged International Equities (relative to unhedged). Across international equities, corporate earnings have proven more resilient than expected. |

| Property and Infrastructure | Neutral | Property and infrastructure as an asset class have been volatile over the previous quarters. Deal volume remains low, and the asset class remains susceptible to interest rate expectations due to the bond-like nature of income returns. We continue to retain a Neutral position. |

| Fixed Interest | Neutral | In-line with changes discussed previously, we have decided to neutralise the overweight in this asset class. Whilst trajectory of interest rates remains uncertain, yields in this asset class today are attractive. |

| Cash | Neutral | Cash yields remain attractive. We have retained cash in our portfolios for buying opportunities should equity valuations reach attractive levels. |

In-line with the outlook, the Investment Committee decided to neutralise our marginal underweight in growth assets; but have elected to maintain our overweight to hedged international equities relative to unhedged. We continue to monitor the geopolitical situation but at this juncture believe neutralising the portfolio over/underweights remains the most prudent course of action.

Yours faithfully,

Allied Wealth Investment Committee

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not consider your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160

It’s no secret that the current financial landscape means that navigating investments, retirement planning, estate management and all the other nitty gritty aspects of your finances can be a bit daunting – and this is exactly where a wealth advisor comes in!

At Allied Wealth, our team is able to provide you with personalised, independent and unbiased financial advice so that you can meet your unique financial goals.

Understanding the role of a wealth advisor is crucial! Essentially they are a financial professional who can provide you with comprehensive guidance on how to create wealth or manage your wealth in the most effective way.

This may include financial planning strategies, retirement planning, tax optimisation, estate planning, investment strategy or anything in between! A wealth advisor basically serves as your partner in your finances.

There are a few key responsibilities of wealth advisors that you may or may not be familiar with, these are some of the key responsibilities of a wealth advisor if you choose to work with one.

Financial planning

A wealth advisor starts by understanding your financial situation, your goals and your risk tolerance. They then work to create customised financial plans that include strategies for those goals – whatever they may be.

Another key responsibility of wealth advisors is to manage investments on behalf of their clients. This could involve creating a diversified portfolio aligned with your goals. The advisor adjusts and monitors your portfolio to respond to market conditions and changes in your financial situation.

Retirement is something that we all look forward to, and helping you plan for a financially stable retirement is a primary goal of a wealth advisor. This could mean estimating your retirement income needs, structuring your withdrawal plans or anything in between.

At Allied Wealth, we pride ourselves on offering some of the best independent financial advice Australia wide. If you’re looking for a wealth advisor and you’re considering a member of our team, here’s just a few of the many reasons you should consider working with us!

When it comes to finding the perfect fit, the right wealth advisor can really be a make or break decision when it comes to your finances. At Allied Wealth, we are committed to guiding you through every step of the way so that you can receive comprehensive advice that is tailored to you.

We have some really exciting news that we are thrilled to announce! Recently, we have been honoured with nominations for two prestigious industry awards that really highlight our commitment to the financial services industry.

First up, we were finalists for the Best Independent Dealer Group at the Australian Wealth Management Awards. This nomination, and us as finalists, recognises our commitment to provide every single one of our clients with independent, client-focused financial advice that is tailored to meet your unique needs.

This recognition is a real testament to the hard work and expertise of the entire Allied Wealth team and their commitment to delivering exceptional financial advice and outcomes to every single one of our Allied Wealth clients, every single time.

As well as that nomination, Allied Wealth’s very own Greg was nominated for the Dealer Group Executive of the Year at the IFA Excellence Awards. Greg’s leadership has been instrumental for steering Allied Wealth in the right direction and he is committed to his clients every single step of the way and the wider Allied Wealth team is so proud to see his efforts and achievements recognised at such a high level.

These nominations reflect our main mission at Allied Wealth – to help our clients achieve their financial goals through independent, unbiased advice and planning. Our nominations and our finalist placing serves as motivation for us to keep raising the bar in the financial services industry, keep getting those nominations and continue to be an award-winning financial advice provider in Australia.

We want to thank all our clients, whose trust and support is a key factor in our success and our journey, we are dedicated to continuing to provide you with some of the best (award nominated!) service in the industry.

Stay tuned as we update our website to proudly display these nomination badges!

If you have any questions or would like to learn more about how Allied Wealth can help you secure your financial freedom, you can contact us today.

Whether you need help with retirement planning, investment advice, wealth management planning or anything in between, our team can help you every single step of the way.

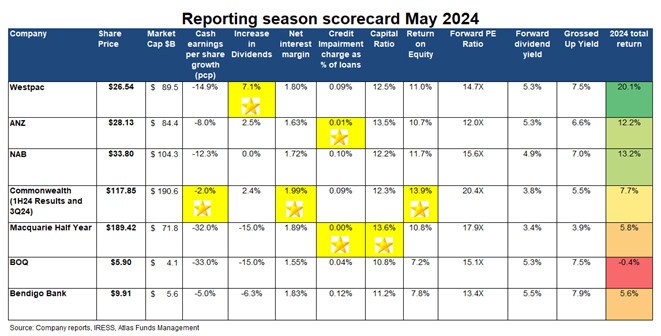

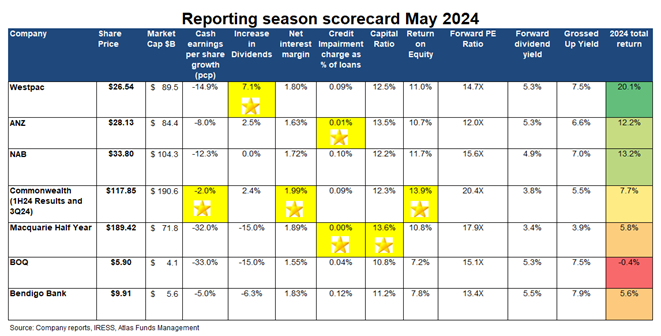

The May 2024 bank reporting season was the mildest and most boring in the past decade, with the major banks all reporting solid results, large share buybacks and very low bad debts. The major banks continue to show their resilience in the face of challenges such as the 2018 Royal Commission into Financial Services, COVID-19 lockdowns, system issues in 2021 from expected zero or negative interest rates, and the "fixed-interest rate cliff" from late 2022 that was forecasted to put the country into a recession as discretionary spending collapsed, defaults spiked, and house prices plummeted.

In this Allied Wealth quarterly, we will look at the themes in approximately 900 pages of financial results released over the past ten days by the financial intermediaries that grease the wheels of Australian capitalism.

Net interest margins are always a major topic during any of the banks' reporting season, with most investors going straight to the slide on margin movements in the immense Investor Discussion Packs. Banks earn a net interest margin [(Interest Received - Interest Paid) divided by Average Invested Assets] by lending out funds at a higher rate than borrowing these funds either from depositors or on the wholesale money markets. Generally, bank net interest margins have recovered from the lows seen in 2022, as when the prevailing cash rate is 5%, it is much easier for a bank to maintain a profit margin of 2% than when the cash rate is 0.1%.

Small changes in the net interest margin significantly impact bank profitability due to the size of a bank's loan book (which ranges from $700 billion to $1.1 trillion) and guide future profitability. Going into this reporting season, many in the market expected a significant fall in the banks' net interest margins due to stronger competition within the mortgage market and increased deposit funding costs. May 2024 saw some downward pressure on interest margins, but less than expected, with management teams reporting a moderation of mortgage competition. Commonwealth Bank again wins the gold star in 2024 with the highest net interest margin.

Gold Star

During the COVID-19 pandemic, Australian interest rates fell to record lows as the RBA established the Term Funding Facility (TFF) to offer low-cost three-year funding to banks. Between March 2020 and when the TFF closed in June 2021, Australian banks borrowed $188 billion at rates between 0.1% and 0.25%, which was then lent as fixed-rate mortgages in 2020 and 2021 at mortgage rates between 1.75% and 2.25% to around 800,000 borrowers. These low-rate mortgages began expiring in mid-2023, converting to variable loans around 5.5%.

With every cash rate hike, the questions became louder about the negative impact of this fixed rate cliff on retail sales, bank bad debts and house prices, with market experts predicting 2023 and 2024 to be very poor years for the banks and retail sales, as borrowers were unable to afford the higher mortgage payments. However, in mid-2024, the economy has proven more resilient than expected, and unemployment remains close to all-time lows. Borrowers and the banks have managed this transition to higher rates, far better than was expected, building up savings buffers. Indeed, despite increased financial pressures, RBA data shows that less than 1% of home loans are in 90-day arrears, a figure that is lower than before the pandemic - RBA Financial Stability Review.

Bad debts have remained low in 2024, with all the banks reporting extremely low loan losses. Macquarie Bank reported the lowest bad debts of 0.00%, with ANZ not far behind with 0.01% loan losses. The level of loan losses is important for investors as high loan losses reduce profits, and this dividend erodes a bank's capital base. This reporting season has translated low bad debts into increased share buybacks and dividends.

Atlas see that the low level of bad debts is a combination of the bank's managing loan book, stronger than expected economic conditions and more conservative lending than we saw from the banks 2000-07. We believe that the loans to developers, property syndicates and troubled industrial companies that went bad in 2008-2010 now sit with non-bank lenders and private debt funds rather than the big four banks.

Gold Star

A feature of the May 2024 banks reporting season was solid dividend growth, with ANZ, CBA, and Westpac increasing their dividends and NAB holding their dividend flat. In the first half of 2024, the big four banks generated $15.6 billion and will return $11 billion to shareholders through dividends or a 71% payout of profits generated throughout the half. Higher dividends reflect the combination of low write-offs from bad debts, minimal new investments (outside ANZ) and high capital levels.

The winner of the star was Westpac, with a dividend increase of 7% or 29% if a special dividend is included. In 2024, all major banks (including Macquarie) will be paying a dividend per share higher than in 2019.

Gold Star

Capital ratio is the minimum capital requirement that financial institutions in Australia must maintain to weather the potential for loan losses. The bank regulator, the Australian Prudential Regulation Authority (APRA), has mandated that banks hold a minimum of 10.5% of capital against their loans, significantly higher than the 5% requirement pre-GFC. Requiring banks to hold high levels of capital is not done to protect bank investors but rather to avoid the spectre of taxpayers having to bail out banks, as has been done in the USA and UK.

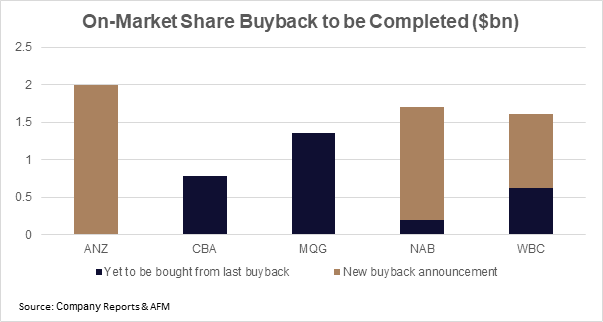

In 2024, the Australian banks are all extremely well capitalised, so much so that ANZ, NAB, and Westpac announced on-market share buyback extensions to return capital to shareholders. During the bank reporting season, NAB announced a $1.5 billion share buyback extension on top of their 200 million remaining from their previous buyback, Westpac announced a $1 billion extension on top of their $600 million remaining from their previous buyback, ANZ announced a new $2 billion share buyback and Macquarie announcing they still have $1.35 billion to buy back from their $2 billion buyback announced in November. For investors, this not only supports the share price in the coming months but reduces the amount of outstanding shares to divide next year's profits.

In addition to buying back shares to reduce capital, all the big banks, including Macquarie, have neutralised their dividend reinvestment plan (DRP), which allows shareholders to take their dividends in additional shares rather than cash. Neutralising the DRP sees the bank buyback shares on-market equivalent to the new shares issued to shareholders. In May 2024, Atlas estimates that this will see additional net purchases of around $900 million in shares from ANZ, NAB, Westpac and Macquarie.

While buying back shares on the market and then cancelling them is positive for shareholders as it reduces the divisor on future bank profits, bank management teams are awarded bonuses based on their return on equity (ROE). Obviously, buying back shares reduces the equity, thus boosting ROE.

Gold Star

Overall, we are happy with the financial results from the banks owned by the Allied Wealth Australian Equity Portfolio in May. The three main overweight positions, ANZ and Westpac, increased their dividends, and Macquarie Bank showed a 49% increase in net profits in the second half, which also guided to increased profits in FY25. All three announced significant on-market share buybacks, which will support share prices.

All banks showed solid net interest margins, low bad debts, and good cost control. Profit growth is likely to be tough to find on the ASX over the next few years, with earnings for resources and consumer discretionary likely to retreat; however, Australia's major banks continue to positively surprise the market with how they have been able to navigate turbulent market conditions. In 2024, the banks will all have cleaner loan books, minimal offshore distractions, and a greater margin of safety than they have had in the past.

Financial advisors play a critical role when it comes to helping individuals to navigate their finances. Whether it’s personal finances, investments, retirement planning or anything in between seeking out the help of an experienced professional can be very beneficial.

Whilst you’ve probably heard the term financial advisor before, there is often confusion about what a financial advisor actually is and what they actually do.

This is our comprehensive guide to what a financial advisor is, what it is they actually do and how they can help you get a better understanding your finances.

In short, a financial advisor is a person who provides guidance and expertise on a range of different aspects of your finances. A financial advisor's main goal is to help their clients to make informed decisions about managing their money, investing for the future and planning for significant life events like retirement.

Financial advisors work closely with their clients to understand their financial goals, risk tolerance and their current financial situation to help develop personalised strategies to help their clients hit their financial objectives.

There are a number of different financial services available when you work with a financial advisor, these are some of the most common services you can expect to see financial advisors offering to their clients.

One of the main things a financial advisor can help you with is to help you build and manage your investment portfolios tailored to your financial goals. This means helping with advice in regards to types of investments, asset allocation and ongoing monitoring to help optimise your returns and manage your risk.

Financial advisors can help clients in creating financial plans that address their financial situation as well as their goals for the future. This can include budgeting, saving, retirement planning, risk management and more. These financial plans can help be the roadmap to help clients achieve their short-term and long-term goals.

Planning for retirement is an exciting and daunting time in everyone's life and it’s a significant part of financial advisory services. Advisors can help clients assess their needs for retirement and help them build wealth and manage their super funds to maximise their income for retirement.

Our team of financial advisors can help you manage your self managed super fund. They provide expert guidance on the creation, administration, and investment strategies for self-managed super funds. If you need some guidance on your SMSF, a financial advisor is a great place to start!

At Allied Wealth, we know how important it is to have personalised financial guidance that is tailored to your needs and goals. Our team of expert financial advisors can help you navigate the financial landscape and reach all your short and long-term financial goals.

If you want to find out exactly how our financial advisors can help you, you can contact a member of our team today to learn more about our comprehensive services and our transparent subscription plans.

If you’ve been looking into seeking professional financial advice but the possible price is holding you back, we hear you! One of the very first questions that people ask themselves when they seek financial advice is, “How much does this cost?” and whilst the cost can vary depending on a number of factors we pride ourselves on transparent pricing!

At Allied Wealth, we know that being transparent, especially when it comes to finances,is crucial, and we aim to offer transparent and comprehensive pricing subscription plans so that you can get expert advice every step of the way.

Here is a comprehensive guide to what factors influence the cost of financial advice and how much you can expect to pay with our subscription plan.

One of the main factors that may influence the overall cost of your financial advice services is how complex your situation is. The cost of independent financial advice can depend on your current financial situation, your goals, your assets and your risk tolerance.

When it comes to providing you with the best financial advice, advisors have to assess your financial situation to provide you with tailored recommendations. If your financial situation is more straightforward, you might require just basic advice. But if you have a more complex financial situation you might be charged at a slightly higher rate due to the increase in work for your advisor.

The range of services you need will also impact the overall cost of financial advice. If you’re only seeking advice on retirement planning, you may pay less than if someone was needing guidance with retirement planning, investment advice and SMSF advice.

At Allied Wealth, our subscription plans are tailored to individuals that require a comprehensive range of services. Our 12-month plans which start at $550 a month include scenario analysis, initial and ongoing advice, quarterly investment updates, bi-annual review meetings and ongoing access to your advice that you can get personalised guidance tailored to your needs without hidden fees.

The pricing structure used by financial advisors also plays a role in determining the overall cost of their services. Some advisors will charge a flat fee for their specific services whilst others might use a percentage-based fee structure.

At Allied Wealth, we think that transparent pricing is key to a great advisor/client relationship. Our subscription plan means you get a fixed monthly fee so you know exactly what you’re paying each month. Avoid hidden charges or expensive surprises and remain focused on achieving your financial goals when you work with our team of expert independent advisors.

To find out more about our pricing structure and the types of financial advice services we offer, you can contact a member of our team today.

If you’re looking for transparent pricing from a team of expert independent financial advisors you have definitely come to the right place!

It’s no secret that there are loads of podcasts out there, and financial podcasts are no exception. But not every finance podcast is created equal, and if you’re an Australian looking for an Australian finance podcast that is relevant to you and your circumstances, you’ve come to the right place!

Gone are the days of having to sit down and read a book or read the newspaper to get all the latest financial news and advice, you can now do any number of things at the same time as listening to your financial podcast. Whether you’re driving, cleaning the house or heading out on a walk – it’s never been easier to get all the latest and greatest finance advice in Australia directly into your ears!

Whether you’re looking for advice on budgeting, investing, superannuation, SMSF advice, shares or something else entirely, there’s guaranteed to be an Australian finance podcast to suit you.

These are some of our favourite finance podcasts in Australia right now!

The Australian Finance Podcast is your guide to sorting out your finances in easy to digest episodes. Hosts, Owen and Kate bring forward actionable strategies and knowledge that you can put into practice to save money and invest better.

With regular episodes you can listen to them all or choose the ones most relevant to you, it’s never been simpler to sort your finances.

If you’re looking for the latest stories, experiences and case studies from Australia’s most innovative property investors – this is the podcast for you. Host Tyrone Shum explores the stories, strategies and advice from real Australian investors.

Whether you’re a budding property investor or you’re more experienced, this is the podcast for you.

If you’re looking for quick, ten-minute bite sized finance news, this is the podcast for you. Daily ten-minute updates on all Australia’s latest finance and business news is delivered by SBS finance Editor Ricardo Goncalves so that you can always stay ahead of the latest developments in the Australian financial landscape.

If you’ve been listening to finance podcasts for a while, chances are you’ve heard of this very popular one. Victoria Devine a millennial money expert and financial advisor shares all her foolproof tips for financial freedom. Whilst it is a podcast that is by a woman, for women – anyone can listen!

If you’re looking for approachable, enjoyable and easy to understand financial advice, She’s On The Money is definitely the podcast for you.

If you’re looking for a podcast to teach you all the money lessons you might have forgotten since school, How To Money is a great one for you. Hosted by a pair of best friends, How To Money aims to teach normal people everything they need to thrive in areas like debt payoff, investing, taxes and more.

If you’re looking for unbiased and jargon-free financial advice, this could just be the podcast you’ve been waiting for.

This is another one for those looking for Australian financial news. The Money Puzzle covers all the important property, business, money and finance news presented by The Australian’s Weath Editor, James Kirby.

If you’re looking for financial news and wealth building advice delivered straight to your ears twice a week, The Money Puzzle could be the perfect podcast.

The Australian Investors Podcast is a bi-weekly podcast that provides intelligent, laid-back advice and information about markets, business, psychology, investments and so much more.

The Australian Investors Podcast is providing the best insights, information and proven strategies to help you invest your time and money. With episodes every Wednesday and Saturday you’ll always have something to learn from the Australian Investors Podcast.

If you’re tired of just listening to podcasts and you're looking for valuable independent financial advice from in-person experts, our team at Allied Wealth can help you. Contact our team today to see how we can help you get your finances in order with independent, unbiased advice.

If you’ve been thinking about setting up a self-managed super fund AKA an SMSF but you’re feeling a bit overwhelmed by everything that is involved – you aren’t alone. Whether you’re looking for expert advice to guide you through opening an SMSF or to help you optimise the performance and ensure compliance of your existing SMSF, an SMSF advisor is the way to go!

There are a number of reasons why you should work alongside an SMSF advisor. With regulations and investment opportunities constantly changing and shifting, having an expert by your side can help you get the most from your SMSF.

If you’re looking for an SMSF advisor, this is our guide to finding the perfect fit for you.

The number one thing you need to do before you start on your hunt for an SMSF advisor is to take the time to really set out exactly what you’re looking for. Do you need help with set-up? Are you looking to help with compliance management or investment strategies? Maybe you need help with all of the above?

The first step to finding the right SMSF advisor is to really understand exactly what you need so you can find someone with the right expertise.

When it comes to checking out potential advisors, make sure their expertise aligns with your goals and your needs. Look for qualified SMSF specialist advisor that has experience in SMSF set-up and management to make sure you’re getting advice from some of the best in the industry.

You’ll want to research the reputation of the SMSF advisors you end up working with. Check out case studies and online reviews from clients to make sure your chosen advisor has a good reputation in the industry and a history of happy clients. If you can’t find anything online, don’t hesitate to try to seek out personal experiences from family members or friends to make sure you’re working with an SMSF advisor you can trust.

One of the most important steps you need to take is to ensure the advisor you choose is licensed and regulated by the Australian Securities and Investments Commission (ASIC). Compliance with regulatory requirements is crucial for protecting your interest and making sure there’s ethical conduct.

Check out the kinds of services that are offered by your team of chosen SMSF advisors. These services might be SMSF advice like SMSF set up, or something else entirely like investment advice, wealth creation advice or retirement planning. Choose an advisor who can provide you the services and support you need tailored to your circumstances.

The number one thing you need to ensure when locking down an SMSF financial advisor is effective communication! You need to ensure your advisor is responsive to your inquiries and concerns and vice versa. Clear lines of communication and regular updates is key to ensuring a successful advisor/client relationship built on transparency and trust.

It doesn’t matter how qualified your SMSF advisor is if you just don’t click! Make sure you choose an SMSF advisor that you’re comfortable with and that you trust. Make sure you’re compatible with your advisor and that you’re comfortable enough to discuss your financial situation as well as your goals and concerns.

When it comes to a financial advisor that really does have your best interest in mind, our team at Allied Wealth is the way to go. By using our helpful guide you have all the right resources you need to find the SMSF financial advisor that will best suit you!

Contact our team today to find out more about what our team of independent financial advisors can do for you in regards to your SMSF.

It’s no secret that the financial advisor industry is a male-dominated one, and if you’re a woman looking for financial advice, it can be daunting to lay your finances on the table with a male advisor. Opening up to a financial advisor doesn’t have to be scary, but if you’re looking to work with a female financial advisor to make that initial meeting feel more comfortable, you are well within your rights to do just that!

Here are our top 5 reasons that you should choose a female financial advisor when you’re looking for independent financial advice.

When it comes to working with a female financial advisor, we know the unique challenges that women face in the financial world. We know that women tend to earn less than men and often take time off work more than their male counterparts to have babies, care for their children or care for elderly relatives.

These two factors alone can make it more difficult for you to save for retirement or reach your financial goals and female financial advisors have a deeper understanding (oftentimes even a firsthand understanding) of these challenges and the ways to best approach your finances and financial goals.

When it comes to investing, women tend to be more cautious and also tend to have different priorities when it comes to their money. A female financial advisor knows these worries and concerns well and they may be able to understand and address your concerns and priorities in a way that a male advisor may not be able to do.

When it comes to sharing deeply personal information, like your financial situation, you may be more comfortable sharing that information woman to woman. This may be particularly relevant in delicate situations like divorce or domestic abuse. It’s easier to trust someone that you relate to, so having a financial advisor that is also a woman may make it easier for you to be more comfortable and more open sharing the details of your finances and your life.

When it comes to sharing information about your finances, particularly the nitty gritty details, it’s important to talk to someone who has experience – even lived experience – in your unique situation. When you work with a female financial advisor, chances are that they have had similar experiences or can relate to your experience more than a male financial advisor may be able to. Working with a female financial advisor who knows exactly what you’re going through whether it be relationship changes, career changes or lifestyle changes can help you to navigate the process easier and in a more comfortable environment.

While we definitely aren’t suggesting men aren’t emotionally intelligent, it’s no secret that women are generally associated with having higher levels of empathy and emotional intelligence than their male counterparts. This is crucial when it comes to communication around sensitive subjects, particularly when it comes to the topic of money.

It’s crucial for financial advisors to handle their clients' situations with empathy and care and you may find you receive a higher level of empathy when seeking advice from a female financial advisor.

We know that finding a female financial advisor can sometimes be difficult, and we pride ourselves on having Jess Brizuela on our team if you’re looking to work with an experienced female financial advisor.

At Allied Wealth we have an experienced team of financial advisors, including female financial advisors, that can help guide you through your finances whether you’re looking for retirement planning advice or investment advice.

Contact us today to find out how our team can help you find the female financial advisor you’ve been looking for!

During February and August every year, most Australian listed companies reveal their profit results, and guide how they expect their businesses to perform in the upcoming year. Whilst we regularly meet with companies between reporting periods to gauge how their businesses are performing, reporting season offers investors a detailed and externally audited look at the company’s financials.

The February 2024 company reporting period that concluded last week displayed stronger-than-expected results in a higher inflationary and interest rate environment. The February reporting season’s dominant themes have been a resilient consumer, strong cost management, moderation in inflation and a positive economic outlook. However, many companies performed very well against the headwinds of higher inflation and interest rates, but not all performed well. In this week’s piece, we look at the key themes from the reporting season that fared last week, the best and worst results and how the Portfolio performed.

Going into the February reporting season, the market was expecting the themes that didn't occur in August 2023, cost inflation, higher interest costs, and slowing retail sales, to happen this reporting season. However, once again, the reporting season demonstrated that many companies have managed a higher inflation and interest rate environment much better than many expected, with around 40% of companies reporting beating market expectations. Looking through the ASX companies that exceeded expectations were in the IT, Consumer Discretionary and Real Estate sectors. Conversely, disappointments were clustered in the Energy, Materials, and Healthcare sectors, primarily related to falling commodity prices and rising costs.

The first dominant theme for the February reporting season was the strength of the domestic consumer. In November 2022, Westpac's economists forecasted a grim year for 2023, the much feared fixed interest rate cliff expected to see unemployment rise to 4.5%, an 8% fall in house prices, bad debts to spike and retail sales grinding to a halt.

However, February 2024 showed continued consumer demand for technology and electronic products, with sales growing across the JB Hi-fi brand. Similarly, with Wesfarmers, Kmart increased profits by 27% as consumers looked to trade down to lower price point options and the success of its Anko brand, which is now stocked in Canadian department stores. Consumers were also willing to treat themselves to fashionable jewellery from Lovisa and 4WD accessories from ARB.

Conversely, with the cost of living increasing, the wagering environment has had a downturn, which saw Tabcorp revenues and active users decreasing across both digital and cash wagering. Similarly, consumers weren't as willing to spend on bedding and furniture at Harvey Norman, with sales falling by 9% in Australia.

Across the major supermarkets, a theme that stood out was that food inflation had moderated throughout the first half and into the first six weeks of the next half. During the half, Woolworths saw average prices for fruit and vegetables decline by 6% and average prices for meat fall by 7%, driven by lower livestock prices and an increased supply of fruit. Paradoxically reporting expanding profit margins in February was a case of poor timing for Woolworths, as it will see the company appear before the Senate Select Committee into Grocery Prices; consequently, its share price declined by 8% over the month.

In contrast, companies with revenues linked to inflation continue to benefit; the best example is toll road operators Transurban and Atlas Arteria, which saw increased revenues from higher traffic volumes and inflation-linked tolls. For a toll road, the most significant cost is interest, with the ongoing costs of operating a toll road once built being minimal. Both toll road companies were very active in extending their loan book from 2020 to 22, during a period of the lowest recorded interest rates in five thousand years of human commerce. For example, in mid-2021, Atlas Arteria sold €500 million of 7-year bonds priced at a coupon rate of a mere 0.17%. While this looks low, in early 2020, the company managed to sell €500 million of bonds, paying no coupons with a negative yield of -0.077%! Effectively, bondholders were paying the company to hold their money, a situation that economists such as Adam Smith or John Maynard Keynes would have never foreseen. Since January 2023, tolls have increased by +7.6% on Atlas Arteria's French toll roads, resulting in profit margin expansion from higher revenues and minimal change in expenses.

During reporting season, a dominant theme that continued through was cost control and cost cutting, with over a third of companies reporting that cost pressures have now passed their peak. JB Hi-Fi cost management surprised markets, only increasing by 5%, despite the retailer facing wage and rent growth pressures. JB Hi-Fi benefitted from staff operating more efficiently and more online sales, with online sales in the last half of 2023 increasing to $736 million, up from $170 million in the same period pre-COVID-19.

On the flip side, some companies saw such costs surge, such as Ramsey Healthcare, which saw their costs increase by over 11% and their profits fall by 40%, driven by labour costs and occupancy costs. Similarly, the miners saw cost pressures and weakening commodity prices, which squeezed margins. Diversified miner South32 had a particularly rough month, with reported profits falling 92% due to higher costs, production issues and falling nickel, aluminium and manganese prices.

Commonwealth Bank provides a good look through the economy during reporting season, with Australia's largest bank holding 16 million customer accounts. Consequently, the banks' financial results and accompanying 231-page reporting suite give investors an insight into the health of the various sectors of the economy. CBA showed minimal bad debts and rising dividends but also that higher interest rates had differing impacts across their customer base. While discretionary spending had been cut back along with savings for customers between 20 and 54, older customers above 55 had increased spending and savings.

Insurers had their best results season since the GFC as they enjoyed higher premiums, lower claims inflation, lower adverse weather events, and sound investment returns. Suncorp expects gross written premiums to increase by low-mid double digits and margins from inflation moderations. Similarly, QBE expects its gross written premium to increase by mid-single digits over the coming year while benefiting from subsiding cost inflation.

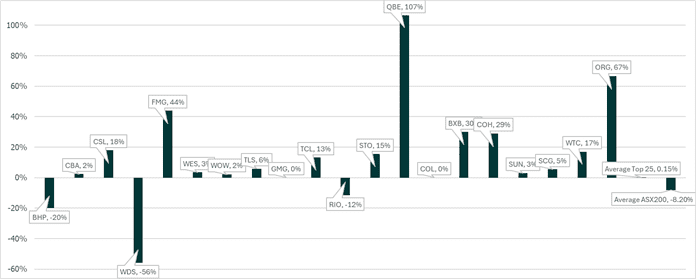

Looking across the top 20 stocks (that reported – the other banks have a different financial year-end), the weighted average dividend increase was 0%. The three companies that reduced their dividends, BHP, Rio, and Woodside, saw weaker commodity pricing.

On the positive side of the ledger, QBE, Origin, and Fortescue offset the cuts, posting solid increases in cash flows to their shareholders. Across the wider ASX 200, dividends declined by -8% in February.

Over the month, Lovisa Holdings, Wisetech Global, Reliance Worldwide, NextDC, and ARB Corporation delivered the best results. Despite the uncertain economic environment, especially around the softening of consumers, these companies were able to grow sales and expand gross margins along with providing optimistic outlooks.

Looking on the negative side of the ledger, South32, Corporate Travel Management, Healius, and Whitehaven Coal reported poorly received results by the markets. The common themes amongst this group were lower commodity prices (South32 and Whitehaven) and slowing sales with high PEs (Healius and Corporate Travel Management).

Before the February 2024 reporting season, conglomerate Wesfarmers would not have been near the top of any investor's picks after a stellar performance in the August 2023 reporting season. Many in the market predicted Wesfarmers' profits would go backwards following a softer economic outlook for domestic consumers and weaker lithium prices. However, the opposite happened with their flagship business, Bunnings, maintaining its earnings and Kmart increasing their profits by +27%, driven by its lowest price position and consumers moving to their Anko brand. Anko has been so successful in Australia that Kmart now offers its Anko product in Canada through the Hudson Bay Company (Canada's Myer). Wesfarmers was up +16% for February 2024.

Overall, we are reasonably pleased with the results from the reporting season, with most of our portfolio companies able to increase earnings and dividends with some reporting record dividends in a more challenging economic environment.

As a long-term investor focused on delivering income to investors, we look closely at the dividends paid out by our companies and whether they are growing. After every reporting season, Atlas looks to "weigh" the dividends that our investors will receive. Our view is that talk and guidance from management can often be cheap, and company CFOs can use accounting tricks to manipulate earnings. However, paying out higher dividends is a far better indicator of how a business will perform in the future. Indeed, in the February reporting season, we saw several companies such as Harvey Norman, South32 and Nine Entertainment Holdings give optimistic outlooks while cutting dividends heavily. This is a mixed message to investors, and we would prefer to follow the cash rather than the words!

Using a weighted average across the Portfolio, our investor's dividends will be +7% greater than the previous period in 2023 significantly ahead of the -8% dividend fall in the wider ASX 200.

The Portfolio’s dividend increase was also ahead of inflation which was 4% over the period, thus maintaining purchasing power for investors that fund their retirement off income. Additionally, every company held in the portfolio was profitable and paid a dividend. Atlas are pleased with the results from the February 2024 reporting season on this measure.

Yours faithfully,

Allied Wealth Investment Committee

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not take into account your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160