When it comes to retirement one of the number one questions we get asked is how much money should I realistically have to retire comfortably? And the truth is, there really isn’t a one-size-fits-all answer for every single individual.

Working out exactly how much you will need for a comfortable retirement depends on a range of different factors including your lifestyle, plans for the future and the number of years you will spend retired living off your retirement fund.

Figuring out exactly how much money you will need to comfortably require also depends on your Super and any investments or assets you have, here’s a rundown on how much you may need to retire, and the factors that you’ll need to consider whilst planning for your retirement.

As per the 2023 Association of Superannuation Funds of Australia (ASFA) Retirement Standard, there are two different budgets for households and living standards per year for individuals aged between 65 and 84 years old.

For a couple, this means that for a comfortable lifestyle you will need about $72,150 per year and if you were happy living a more modest lifestyle, you would need roughly $47,000 per year.

These figures are obviously a bit less if you’re a single, with singles needed around $52,000 per year to live comfortably and around $34,000 a year to live a more modest lifestyle.

If you’re not quite sure what the difference between a modest lifestyle and a comfortable lifestyle is, think of it this way: A modest lifestyle is considered better than living on the age pension, but a comfortable lifestyle means you have a good standard of living and can partake in a range of leisure activities as well as international, and domestic travel.

When it comes to retirement planning and figuring out how much money you’ll need to retire, it ultimately is a very unique and personal thing that also depends on how you would like to live and your lifestyle expectations for retirement.

When trying to figure out how much money you will need to retire, it would be best to figure out exactly how much money you spend on everyday items, recreational activities and any hobbies you may have to factor those things into your considerations.

Obviously the amount of money you will need depends on how long you are planning to be retired, for example if you plan to retire when you are 65, it’s likely you’ll live for at last another 20 years so you will need to have enough funds to cover yourself and your lifestyle for at least that amount of time, plus some wiggle room!

The money you use during your retirement doesn’t solely come from savings you have built up alone, there are a number of different sources you might receive money from during your retirement.

One of the number one things you need to know when planning your retirement is how much Super you have in your Super fund as this will generally be a very large part of your retirement savings.

Depending on your individual circumstances you may be eligible for a full or part age pension during your retirement. You will need to check the eligibility criteria though as some individuals may not be entitled to any form of government assistance or pensions at all.

There are a few different ways you can get funds to retire, whether it’s downsizing your home, selling investment properties or shares or using money you’ve saved in a savings account. If you have received any money in inheritance from your family over the years you may also be able to use this to fund your retirement.

If you want to chat about your unique financial situation ahead of your retirement, seeking independent financial advice from a trusted advisor is a great place to start.

If you’re facing financial difficulty ahead of retirement, there are a few different ways you can get your retirement on track. Having an idea of your current and projected retirement savings is a great place to start so you can work on improving your overall financial situation. The sooner you start putting money aside for retirement, the easier it will be for you to reach the financial goals you have for retirement.

If you need any further guidance on retirement planning or how much money you should have for retirement you can contact a member of our team at Allied Wealth today to see how we can help you reach your retirement goals!

As we begin 2024, we want you to know what a privilege it is to serve as your advisor. Hopefully each quarterly newsletter gives you some insights into our thinking and its evolution as we are confronted with new information and ideas in an ever-changing financial landscape. As always, we strive to maintain a balanced approach with awareness of both upside return and downside risks.

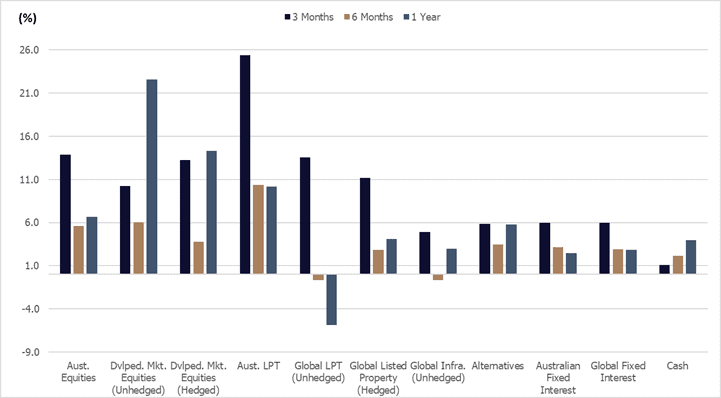

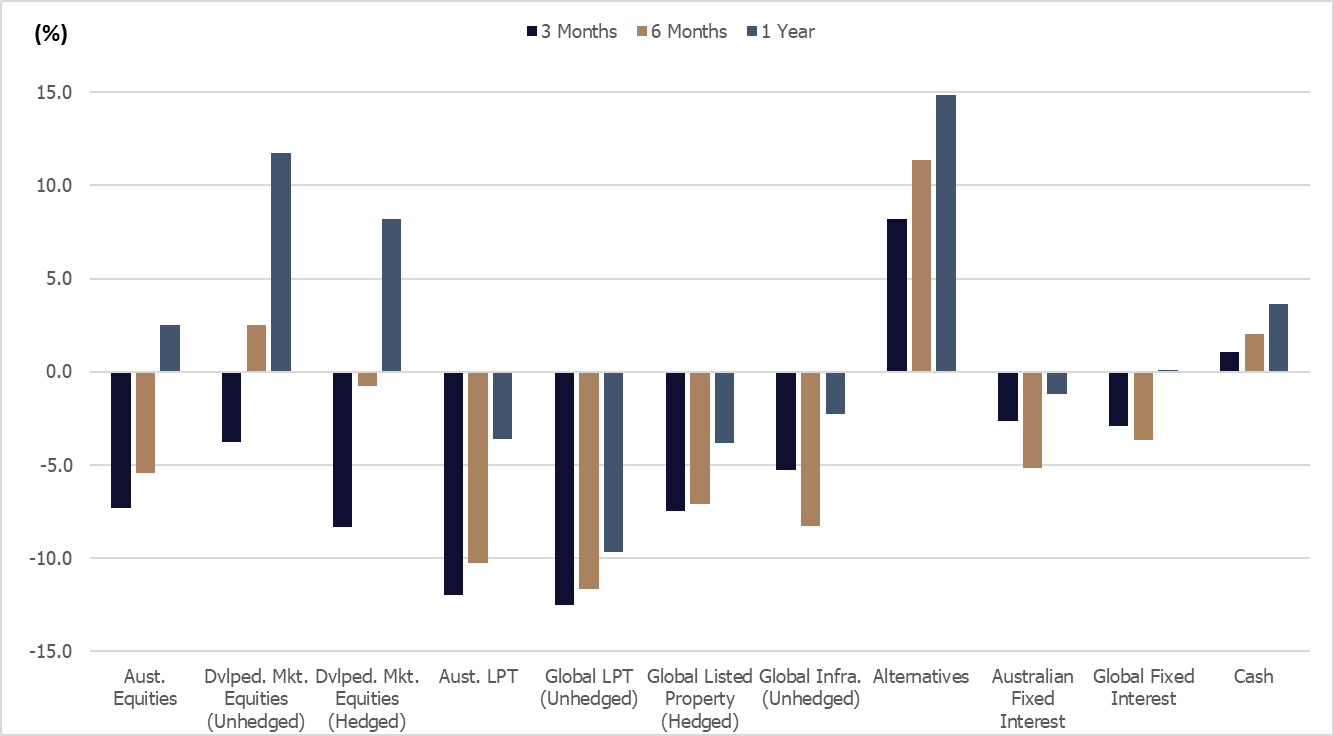

Asset class volatility has continued into 2024, with large return variations observed quarter-on-quarter. Indeed, we have seen correlated asset class performance over 2023 and we think this behaviour will likely continue over the short term. Over the 3-months to January 2024 all asset classes printed positive, driven primarily by market expectations of policy rate cuts over the first half of 2024.

Source: Allied Wealth, Morningstar.

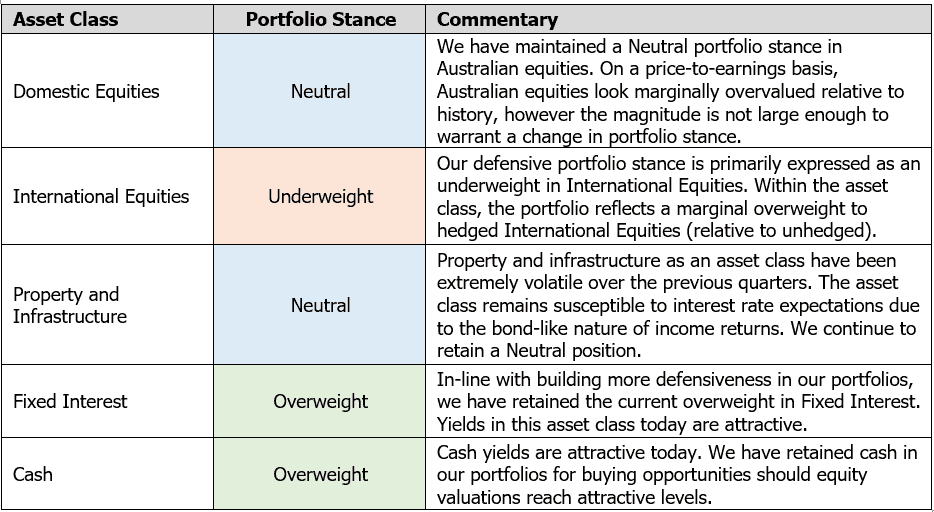

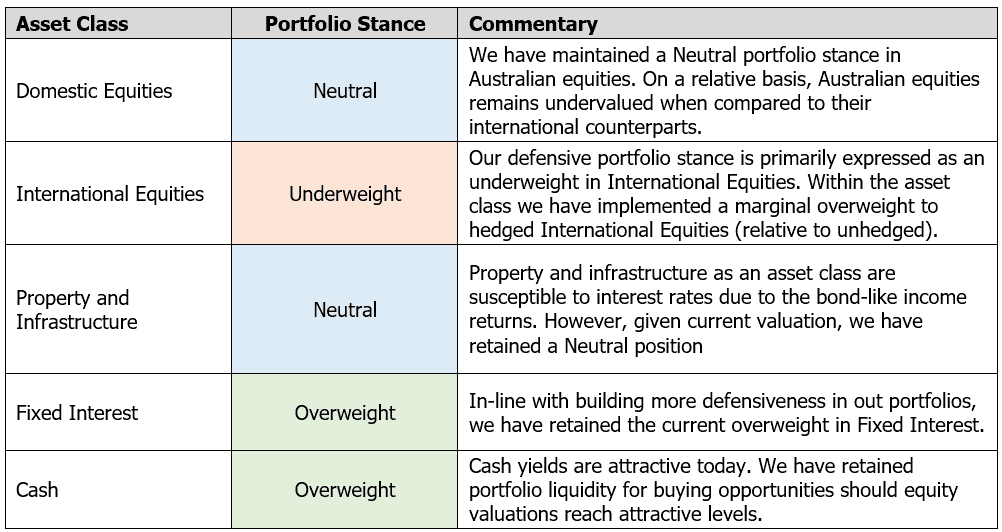

Coming into Q4 2023, we implemented an overweight allocation in hedged international equities relative to the unhedged position. This decision contributed to performance as the Australian Dollar strengthened over the period. Over the quarter, portfolios have maintained a marginal defensive bias expressed as an underweight in growth assets in favour of defensive assets – this position has marginally detracted from relative performance over the quarter. The combined asset allocation decisions are net positive and additive to long-term portfolio returns. While we are pleased with the results, we would emphasize that the asset allocations decisions have been made both from the perspective of risk mitigation as well as alpha generation.

Source: Allied Wealth, Morningstar. Note: Returns are based on an asset allocation index returns which do not include manager and advice fees so actual portfolio returns will vary. The purpose is to determine if our tactical asset allocation decisions are adding value over the Strategic Asset Allocation for each model.

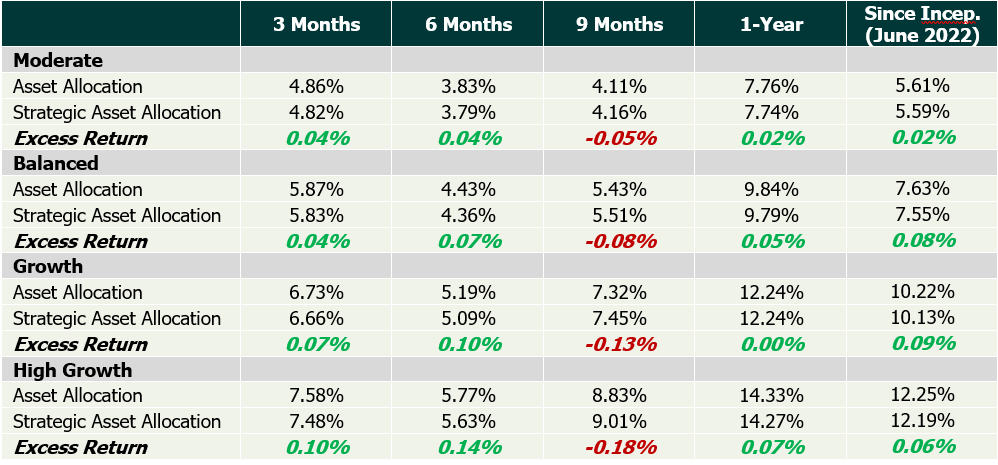

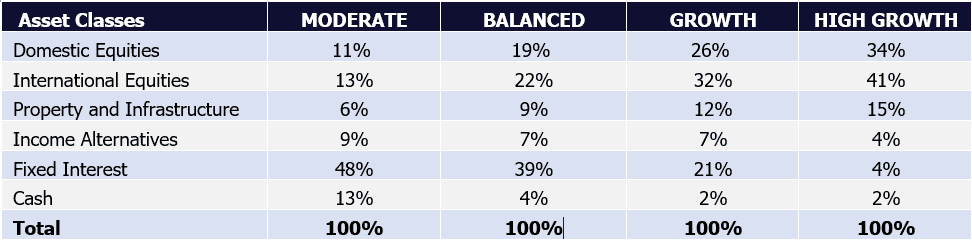

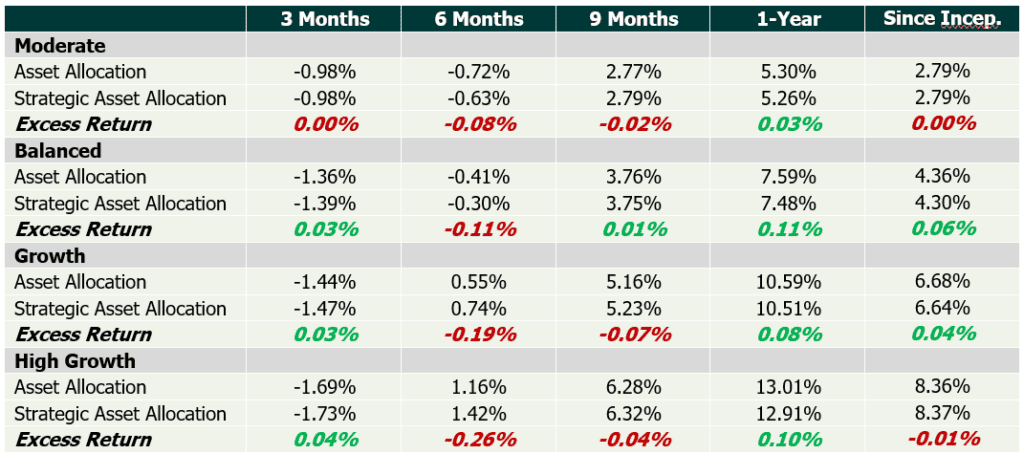

Strategic Asset Allocation Review

In Q4 2023, we conducted a Strategic Asset Allocation (SAA) review of client portfolios across the risk spectrum – Moderate, Balanced, Growth and High Growth. Review includes an assessment of our current Capital Market Assumptions and long-term implications for the baseline SAA.

Our analysis of asset class returns and risks suggests that while there are short-to-medium term market considerations of note, the relative attractiveness of asset classes have not changed over the long-term (20-years forward). Structurally, we see a rise in income yields across asset classes, more so in bonds and credit compared to equities. The attractive level of income has resulted in an increased allocation to Income Alternatives across Moderate, Balanced and Growth portfolios.

One of the key themes discussed at the Investment Committee was narrow market representation. Looking through the market indices we note that positive performance in international equities was primarily driven by strong performance in a small number of large-cap tech stocks (Microsoft, Google, Nvdia, Meta, Apple and Amazon). While there is an argument to be made that large-cap tech is overvalued, we have seen positive earnings growth which continues to support the lofty valuations. However, we note in most cases (exception being Nvidia) a material contribution to earnings growth have been job cuts in the second half of 2023.

The AI boom remains the gift that keeps on giving. Despite record number of lay-offs in the tech sector, companies continue to invest in AI and data processing which has led to strong demand for both software and hardware. This trend has also percolated across property and infrastructure. We have seen substantial investments in data centres and energy infrastructure, supported by new equity and debt raisings. Investors continue to be extremely bullish on these themes coming into 2024.

We believe that central banks globally are mostly at the tail-end of their hiking cycle. Tight monetary policy has led to softening of economic conditions and moderation in inflationary pressures. Inflation remains on the higher end of the target range at around 3%, and we expect this to continue over the first half of 2024.

Investor sentiment remains too bullish for our liking. At this point, equity market valuations are expensive but as history indicates, expensive valuations may persist over long-periods of time. Our analysis suggests that equity valuations today include an expectation that interest rate will fall in H1 2024 followed by earnings growth coming into H2 2024. This thesis at current valuation does not leave much room for error and thus we have remained cautious.

Geopolitical conflict continues to be an ongoing theme. With the US presidential elections in November 2024, primaries have already commenced. Polling and voting to date suggest the upcoming election will be a Trump vs Biden showdown. Irrespective of which candidate wins, we expect further escalation of trade conflict between US and China.

Following the investment committee discussion, members agreed to retain the current asset allocation stance which reflects 1) a marginally defensive stance overweight cash and fixed interest in favour of an underweight in international equities and 2) within international equities, an overweight in hedged international equities relative to unhedged. Despite the appreciation of the Australian Dollar (relative to US Dollar and Euros), current valuations still look cheap relative to history.

In-line with the outlook, the Investment Committee decided to maintain our marginal underweight in growth assets in favour of an overweight to defensive assets; and an overweight to hedged international equities relative to unhedged. Given the current market environment we have thought it appropriate to maintain the cautious stance but will look to reassess our position should it be warranted.

Thank you once again for your continued trust and confidence. We wish you a fruitful and prosperous 2024.

Yours faithfully,

Allied Wealth Investment Committee

What sets Allied Wealth apart

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

General advice warning

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not take into account your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160

If you’ve been thinking about starting your financial planning journey, or you are just looking for some financial advice to see if you’re on the right track, seeking out a financial advisor is a wise decision. Financial advisors can help you plan and manage your finances so you can stay on top of your finances and help to plan for your future.

At Allied Wealth, our team of professional financial advisors provide independent financial advice to help people in a range of different situations with different financial goals. Whether you’ve worked alongside a financial advisor before or you’re new to the industry, these are our top benefits for working with an experienced financial advisor.

One of the most beneficial things about working with a financial advisor is that they can help you build a financial plan that is tailored to you and your goals. A financial advisor can help tailor a strategy to your goals and your risk tolerance as well as helping to provide advice on investments.

Financial advisors work with you to help you create strategies that can secure your financial future, if you’re not sure where to start, a financial advisor is the perfect place.

It can be difficult to navigate your finances but a financial advisor can help you to understand your finances and help you set and reach financial goals and milestones that you may have for the future.

Financial advisors can help you to understand your assets and manage investments so that you can get the most out of your finances.

One of the most important things you can do to set yourself up for the future is to plan for your retirement and a financial advisor can help you to make sure you have everything you need to retire comfortably when the time comes.

A financial advisor can help you on your retirement planning journey by helping you to manage and optimise your financial resources and investments so that you are completely set up for the future and ensure you have the lifestyle after retirement that you’re looking for.

Whilst financial advisors can’t predict the future, they can help you stay prepared for unexpected changes as a result of life events or market fluctuations. Financial advisors can help you stay on top of your finances even during injury, illness, property damage, market dips or career changes so that your finances are always future-proofed.

Our team of experts work to help you organise your finances so that you are always prepared no matter what life may throw your way!

Financial advisors know the financial landscape better than almost anyone, and with that comes an in-depth understanding of investment opportunities. Financial advisors can help you assess your risk tolerance and the necessary finances you need when it comes to investing.

Investments are a great way to future-proof your finances and our team can help you discover what investment opportunities will be best for you and your unique financial goals.

Above all else, working with a financial advisor means you can build a long-term relationship with a dedicated expert who knows your specific situation and is committed to helping guide you towards the best outcomes for you.

Above all else, one of the best benefits you get out of working alongside a financial advisor is a partnership with a trusted and experienced expert who knows your personal situation and your unique goals that works with you to secure the financial future you’ve always dreamed of.

To partner with one of our experienced independent financial advisors you can contact a member of our team today!

When it comes to the best age to start saving for retirement, it really is right away and if you’re asking yourself questions about when you should start saving for retirement the simplest answer is right now.

In an ideal world you should start planning and saving for retirement in your 20s so that you have ample time for your investments to grow before you reach retirement age. If you’re past that age though and you can feel retirement looming, it’s important to remember that it’s never too late to start putting money aside for retirement.

Here are some of our top tips for starting your retirement planning and beginning saving for retirement, no matter your age!

Regardless of your age, having a retirement saving strategy in place probably won’t work for you unless it is easy and seamless. One of the simplest ways to save for retirement is to make it automatic.

The truth is if you have to manually move money into a retirement savings fund every single time you get paid, it probably won’t happen, but setting up an automatic transfer every time you get paid is an easy way that will ensure you are putting funds away every pay.

Chances are good after a few paychecks you won’t even notice the money coming out of your account but you will be building up an ample retirement fund without even realising it!

When it comes to budgeting, most of us do have some wiggle room for some extra savings in our budget. When you take a look at your spending, ask yourself if there are any aspects of your spending habits that you can scale back to replace with saving for retirement.

It’s important to make sure that you’re only saving the amount you can afford as any unreasonable or unrealistic savings will make it much harder to keep up long term. By including your retirement savings in your budget, you get into the habit of putting money away for your future.

Visualise the life you want for yourself in retirement, whether you’re wanting to put aside a large sum for retirement to help set yourself up early or you want to save a couple extra dollars a week – rethinking your budget to include retirement savings will help you to get where you need to be for your future!

When it comes to saving for retirement, especially if you're a long way away from retirement age, it can sometimes feel like more of a hassle than it’s worth – but keeping track of your progress is a great way to help combat those feelings. It can be very satisfying to see your retirement savings grow as you put more into them. Whether you are saving in an account or you’re adding extra into your Super fund each month, keep an eye out for your statements.

Measuring your savings progress will help you stay motivated and that’s the number one thing you need when it comes to long-term saving goals. Staying motivated is the key to staying on track and keeping track of your progress is the perfect way to improve your morale and your motivation.

Whether you are in your 20s just starting your retirement savings journey or you’re a bit older but have neglected your retirement savings – it’s never too late to start! Our team at Allied Wealth can help you when it comes to retirement planning and financial planning for the future.

Our team can help you prepare for the future so that you can have a comfortable and financially free future even in retirement!

Contact a member of our team today to see exactly how we can help you to future-proof your finances!

If you’ve been hearing FIRE AKA financial independence, retire early floating around but you aren’t quite sure what it all means, you aren’t alone. The FIRE movement has gained traction in previous years and if it’s something you’ve been considering adopting but you’re not sure how, this guide is for you.

Our team of experts at Allied Wealth have extensive experience in the world of retirement planning and we have broken down where FIRE came from and what exactly it is.

FIRE is a movement of people that are committed to a life of extreme saving in the hopes to retire far earlier than other individuals may be able too. It’s not known exactly where FIRE originated, but a core premise of the movement is that you should be evaluating every single expense in terms of the number of hours you had to work to pay for those expenses.

The FIRE movement aims to get individuals to retire early, instead of the regular retirement age of 65, the FIRE movement encourages people to dedicate a majority of their incomes to savings so that they can retire and live off their savings years before they reach the traditional retirement age.

FIRE is an extreme saving lifestyle that encourages people to save up to 70% of their yearly income. When their savings reach 30 times their yearly expenses, they are able to leave their jobs or retire all together.

The movement also encourages people to make small withdrawals from their savings after they retire early, roughly 3-4% of the overall balance a year. This requires diligence and extensive budgeting to ensure the success of their efforts.

You wouldn’t be alone in thinking that FIRE is designed for individuals who get a substantial income and can afford to save a majority of their salary and if you’re trying to retire by your 30s or 40s, that’s probably true. BUT there is also a lot to be learnt from the movement that can help people save for their retirement and achieve an early one, even if it isn’t quite as early as retiring in your 30s.

There are three variations of the FIRE movement, Fat Fire is a more laid-back approach that encourages people to save more while giving up less. Lean FIRE will require individuals to be devoted to a very minimalist lifestyle and Barista FIRE which is for people wanting to quit their 9-to-5 and are willing to cut back on their spending and only work part time.

At Allied Wealth we are committed to providing you with a financial plan that best suits your needs, goals and expenses. If you’ve been considering undertaking the FIRE movement as part of your retirement planning, contact us today to find out how we can help you achieve your goals and plan for your future.

If you’re new to the financial planning world, you’ve probably heard the terms “independent financial advisor” and “financial advisor” thrown around a lot and also often used interchangeably which can be confusing if you’re new to the financial planning landscape.

Understanding the differences between these two roles is crucial in order to help you make an informed decision about the type of financial expert you should choose that will best suit you and your needs.

The key difference between a financial advisor and an independent financial advisor is their independence. If you’re looking for financial advice that isn’t associated with banks or financial institutions an independent advisor is the way to go! Independent financial advisors don’t have limitations on the products and services they can recommend so their advice is unbiased and aligns with your financial goals.

Financial advisors may have a vested interest in recommending specific products or services that they are affiliated with or that are offered by their employer. Independent financial advisors have the freedom to recommend products and services from a huge range of providers so your needs are always met rather than trying to meet a quota for a financial institution.

Independent financial advisors are more known to be client focused, taking the time to understand your individual needs and goals. It’s a personalised approach that allows them to tailor their advice to you and your specific circumstances whilst financial advisors may have to offer more generalised advice due to guidelines put in place by their employers.

The cost and fee structures can vary from financial advisor to independent financial advisor. This may be because financial advisors may earn a commission based on products they sell. Our independent advisors work to be completely transparent with our fees and you can be sure that the way we charge is not at all influenced by any commissions.

When you’re choosing between a financial advisor or an independent financial advisor it all comes down to you and your financial goals. At Allied Wealth we offer you the expertise of independent advisors that are completely committed to your financial growth, independence and transparency.

Understanding the difference between independent financial advisors and financial advisors is crucial when it comes to making an informed decision that best benefits you.

Equity markets rallied over the first half of 2023 but lost steam coming into September and October. Over the 3-months to October, all asset class performance was negative except for Alternatives and Cash. While recent market movements have vindicated the defensive positioning taken in Q2 2023, we remain cautious on both the upside and downside going forward.

Markets have remained volatile over the year and the last few weeks of quarter four have not been an exception. For us this highlights the level of disagreement embedded in the investment views held by both institutional and retail investors.

Source: Allied Wealth, Morningstar.

Please note that asset allocation performance calculations have been conducted as of September 2023.

Portfolios currently maintain a marginally defensive asset allocation stance. As was discussed in the last newsletter, the decision reflects a focus on risk management rather than profit maximisation. This position has proven prescient as growth assets have underperformed defensive assets over the quarter.

Source: Allied Wealth, Morningstar. Note: Returns are based on an asset allocation index returns which do not include manager and advice fees so actual portfolio returns will vary. The purpose is to determine if our tactical asset allocation decisions are adding value over the Strategic Asset Allocation for each model.

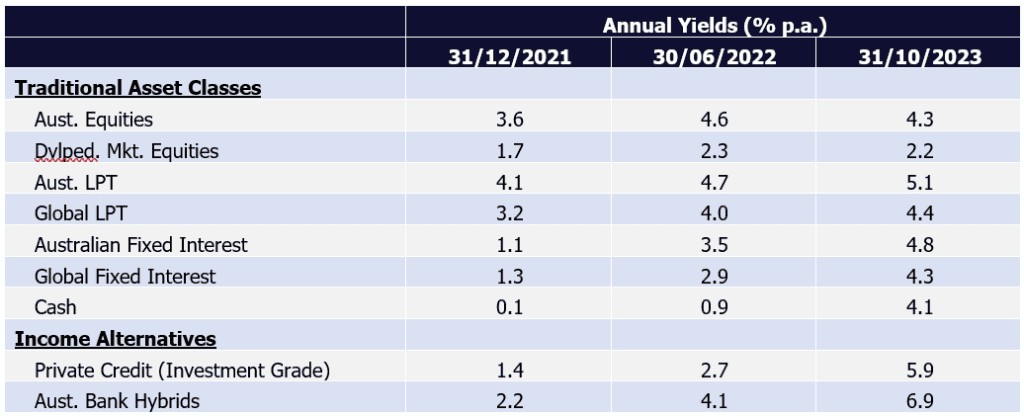

Structural Market Changes – The Returns of Income

Over the past year, rising interest rates have meant a higher income return across defensive asset classes as well as select Alternative asset classes. Where equities have (over the last 10 years) provided a higher income yield compared to bonds, the recent hiking cycle has seen income levels across multiple asset classes rise materially.

Notes:

Dividend yields have been used for equities; yield-to-maturity for bonds

For private credit and Aust. bank hybrids yield have been calculated as a spread plus cash

Comparing yields at the end of October 2023 to December 2021, we see a material increase in yields across Fixed Interest, Cash and Income Alternatives. In some cases, yields exceed dividend yields for equities. Another important point to note is that these asset classes also exhibit lower volatility of capital relative to equities which makes for an attractive investment proposition particularly for investors with lower risk tolerance. As an investment committee, we have begun discussing the implication for client portfolio and expect this to be an important consideration in the upcoming Strategic Asset Allocation review.

Investment Outlook & Strategy Implications

We continue to maintain a cautious asset allocation stance. We see a combination of growth headwinds in the medium-to-near term. The impact of higher interest rates is working through the economy, and we have seen signs of corporate earnings under pressure. Consumers have started to feel the pinch and have adjusted their spending accordingly.

Geopolitical conflict has been a theme well covered in all our publications as well as internal discussions. The escalation of conflict in the middle east represents a grave humanitarian crisis with implications for oil prices. However, the impact of the conflict on global GDP currently remains minimal. It remains too early to tell the secondary or third-order effects and we continue to monitor the situation as it develops.

Market movements across equities and bonds suggest market participants remain glued to central bank commentary. While any indication of a “pause” in policy rates is cheered on by investors and may lead to a short-term equity rally, we believe fundamentals are likely to deteriorate further before improving. Despite falling equity prices in the recent months, we continue to view the asset class as overvalued especially when earnings momentum and economic fundamentals are considered. Based on our current assessment, we would like to see a further 5% to 10% fall in prices before adding back to underweight positions.

Within international equities, we have made some minor allocation changes resulting in a marginal overweight to hedged international equities (relative to unhedged). Over the preceding quarters we have seen the Australian dollar materially weaken relative to the US dollar and Euros. Based on our analysis, the Australian dollar currently trades cheaply when compared to other development market currencies. Our experience with FX suggests that while mean reversion is likely, this can happen over an extended period. Current valuation provides a good entry point, and we expect to hold on to this position over the medium term.

Bottom-up market observations

Reporting Season Scorecard

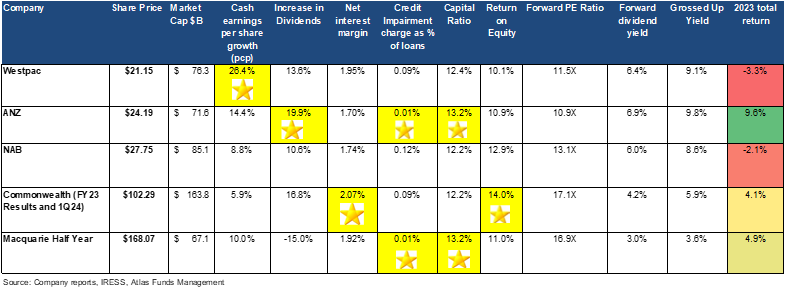

The last four years have been very eventful for bank shareholders, with each year bringing a new set of worries predicted to bring the banks to their knees. 2020 saw an emergency capital raising from NAB (some of which was used to pay the dividend) and Westpac missing their first dividend since the banking crisis of 1893, as experts forecasted 30% declines in house prices and 12% unemployment! Then, 2021 saw the banks grappling with zero interest rates and APRA warning management teams about the systems issues they may face from zero or negative market interest rates expected to come in 2022. In 2022 and 2023, the concerns have switched to the impact of a 4.25% rise in the cash rate on bad debts and the looming fixed interest rate cliff that would see retail sales and house prices plummet.

In this Allied Wealth quarterly, we will look at the themes in approximately 900 pages of financial results released over the past ten days by the financial intermediaries that grease the wheels of Australian capitalism.

Low Bad Debts

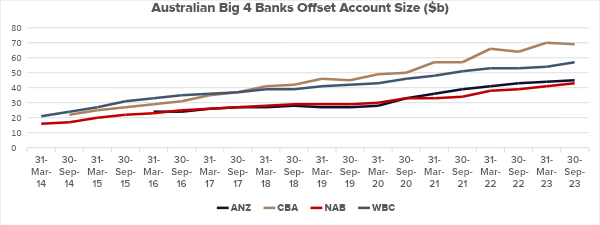

From May 2022, Australia's official cash rate climbed from 0.10% to 4.35% across 13 different rate hikes. Every time we had a cash rate increase, the first question was how it would impact consumers and whether bad debts would rise sharply and house prices would collapse. What we have seen over the last year is that employment in Australia has remained remarkably robust in a tight labour marketplace. This has seen consumers being able to reallocate funds from discretionary or non-necessity spending to being able to fund their home loans. Additionally, we have seen a substantial increase in offset account balances that have risen rather than fallen, with $5 billion being added since March 2023.

Bad debts remained low in 2023, with all banks reporting negligible loan losses; ANZ and Macquarie reported the lowest level, with loan losses of 0.01%. To put this in context, since the implosion in 1991 where, banks grappled with interest rates of 18% and considerable losses to colourful entrepreneurs such as Bond, Skase et al. Since then, loan losses have averaged around 0.3% of outstanding loans, and the banks price loans assuming losses of this magnitude.

The level of loan losses is important for investors as high loan losses reduce profits and, thus, dividends and erode a bank's capital base. Conversely, the very low losses in 2023 have translated into record dividends and billion-dollar share buybacks.

Show Me The Money

While the big Australian banks are sometimes viewed as boring compared with the biotech or IT themes du jour, what is exciting is their ability to deliver profits in a range of market conditions. In 2023, the banks generated $32.7 billion in net profits after tax. This saw dividends per share increase by an average of 15% per share, with all banks except for NAB now paying out higher dividends than they did pre-Covid 19. The star among the banks was ANZ, which raised dividends per share by 19%!

Well Capitalised

Capital ratio is the minimum capital requirement that financial institutions in Australia must maintain to weather the potential loan losses. The bank regulator, the Australian Prudential Regulation Authority (APRA) has mandated that banks hold a minimum of 10.5% of capital against their loans, significantly higher than the 5% requirement pre-GFC. Requiring banks to hold high levels of capital is not done to protect bank investors but rather to avoid the spectre of taxpayers having to bail out banks. In 2008, US taxpayers were forced to support Citigroup, Goldman Sachs and Bank of America, and British taxpayers dipping into their pockets to stop RBS, Northern Rock and Lloyds Bank going under. The Australian banks were better placed in 2008 and did not require explicit injections of government funds; the optics of bankers in three-thousand-dollar Armani suits asking for taxpayer assistance is not good.

In 2023, the Australian banks are all very well capitalised and have seen their capital build. This allows the banks to return capital to shareholders in the form of on-market buybacks. During the bank reporting season, Macquarie announced a $2 billion dollar on-market buyback, Westpac announced a $1.5 billion share buyback, CBA announced a $1 billion share buyback, and NAB announced they had a remaining $1.2 billion share buyback. For investors, this not only supports the share price in coming months but reduces the amount of shares outstanding to divide next year's profits by!

Our View

Overall, we are happy with the financial results in November from the banks owned by the Concentrated Australian Equity Portfolio. The three main overweight positions, Commonwealth Bank, ANZ and Westpac, all increased their dividends, which is a crucial signal indicating improving prospects and board confidence in the outlook. All banks showed solid net interest margins, low bad debts and good cost control. Profit growth is likely to be tough to find on the ASX over the next few years, with earnings for resources and consumer discretionary likely to retreat; however, Australia's major banks look to be placed in a good position in current turbulent markets.

Every investment decision is not undertaken lightly and is based on investment research, sized by our conviction. In-line with the outlook, the Investment Committee has decided to maintain our underweight in growth assets in favour of an overweight to defensive assets. Apart from a marginal overweight in hedged international equities within the asset class, no other allocation changes have been made.

Yours faithfully,

Allied Wealth Investment Committee

What sets Allied Wealth apart

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our independent financial advice services.

General advice warning

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not take into account your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160

When you’re nearing retirement age, it’s vital to understand your finances so you can live comfortably during the later years of your life. At Allied Wealth we know how complex and confusing it can be to understand all the nuances of financial planning for retirement. We know there are a different set of challenges faced by individuals who are planning to retire and our independent financial advice is tailored to make your retirement financial planning as easy to navigate as possible.

If you’ve been thinking about retirement for a while now but you’re just not sure where to start on your financial planning journey, you aren’t alone – and we are here to help! Financial planning for retirement is crucial and we know there are a whole range of considerations you have to keep in mind.

When you’re starting on your retirement financial planning journey you’ll need to regularly assess your financial situations as well as your ongoing needs and goals.

At Allied Wealth we know that there are different financial concerns for Australians that are at different stages of their lives which is exactly why we provide retirees with specialised guidance.

One of the biggest concerns for Australians considering retirement is ensuring that you have the funds to be comfortable and secure. At Allied Wealth we do it all, from evaluating your current savings to helping you invest, our advisors help you every single step of the way.

It’s no secret that as you age, the cost of health care needs to be included as a significant part of your budget. At Allied Wealth we can help you plan for these potential costs to ensure you have the finances to cover any medical procedures or appointments and the cost of private health insurance. Planning for health care expenses (whether expected or unexpected), ensures you have the finances to handle whatever life may throw at you!

When you are in the midst of planning for your retirement, estate planning cannot be overlooked! We can help you to create a comprehensive plan for your estate that respects exactly what you want and protects your assets. Our advisors can help you with your estate planning so you can pass on your assets to future generations.

Navigating possible tax benefits within retirement can be a difficult thing to do, but it’s an important part of any financial planning process. We can help you explore tax-efficient strategies that help you to make the most of your finances. Our advisors provide you with personalised insights and potential tax benefits that can make a significant difference to your financial situation.

When you’re beginning to plan for retirement, checking over your finances and ensuring they align with your future goals is crucial. With Allied Wealth at your side, you can handle your retirement with confidence knowing that you have experienced advisors who provide personalised guidance to help you navigate the Australian financial landscape.

Key Themes

During February and August every year, most Australian listed companies reveal their profit results, and most guide how they expect their businesses to perform in the upcoming year. Whilst we regularly meet with companies between reporting periods to gauge how their businesses are performing, companies open up their books during reporting season to allow investors a detailed look at the company's financials. As company management has been on "blackout" (and prevented from speaking with investors) since mid-June, share prices in the six weeks leading up to the result are often influenced by rumours, theories, and macroeconomic fears rather than actual financials.

The August 2023 company reporting period that concluded last week displayed stronger-than-expected results in a higher inflationary and interest rate environment. The dominant themes of the August reporting season have been higher interest repayments, higher input costs and a weaker Australian dollar. Many companies were able to weather these headwinds and deliver some strong results, and others got caught in the headwinds. In this week's piece, we look at the key themes from the reporting season that finished last week, along with the best and worst results and the corporate result of the season.

Better than expected

Going into the August reporting season, the market expected the profits to fall sharply due to the combination of cost inflation, higher interest costs and slowing retail sales from domestic consumers under pressure from higher mortgage rates. However, the reporting season showed that many companies were able to manage the current economic environment better than expected, with earnings beating expectations outnumbering companies missing expectations by a ratio of 5:3. Looking through the ASX companies that exceeded expectations were in the telco, IT, consumer discretionary and financial sectors. Conversely, disappointments were clustered in the consumer staples and healthcare sectors.

Higher interest rates - Good and bad

One of the main themes over this reporting season was how each company would be able to handle a rising interest rate environment. Since 2008, companies globally have enjoyed declining interest rates, which have seen the interest cost line on the Profit and Loss statement decline, thus boosting earnings. However, since April 2022, the cash rate has increased from 0.1% to 4.1%. August 2023 was going to be the first reporting season, with sharp increases in financing costs taking a bite out of company profits.

Aurizon (nee Queensland Rail), Australia's largest rail freight operator, underwent a large acquisition last year, adding close to $2 billion in additional debt. When combined with an increase in interest rates, the rail company saw its interest expense explode by 84%, dragging earnings down. Similarly, we have seen financing costs increase for the more highly geared listed property trusts such as Charter Hall Long WALE REIT, which saw financing costs increase by 56%. Retailer Harvey Norman is another company that has seen a large increase in financing costs of 76% due to having to take on more debt to fund more capital expenditures.

Conversely, the insurers all reported strong earnings results courtesy of finally earning an income return above zero on their "insurance float". In addition to profits made via underwriting insurance, insurance companies receive premiums upfront and pay claims later, which gives the company a cost-free pool of money that can generate investment profits for the benefit of shareholders. This pool constantly has inflows from premiums and outflows from claims, but the aggregate amount tends to remain constant. For the last several years, with rates close to 0%, insurers were earning close to nothing for their multi-billion-dollar investment floats. However, with rising interest rates, QBE Insurance earned US$662 million on its US$27 billion float in the first half of 2023. Conversely, the company made only US$382 million in all of 2021.

Input cost inflation

Over the past year, wages have risen across many sectors in Australia due to a combination of maintaining real wages in the face of higher inflation and a tight labour market with unemployment the lowest since the early 1970s. In August, cost inflation was seen very clearly in the profit results of the big miners. BHP reported higher production costs for FY2023 with diesel, explosives, machinery, and labour increasing costs by 10% over the year and expects higher costs to remain in FY2024.

Retailers Coles and Woolworths both saw higher costs of doing business in FY2023 due to higher minimum wage awards and cost inflation. Additionally, Coles lost $60 million in "shrinkage" (theft) during the second half, which alarmed investors and saw the company's share price fall. To combat this, Coles plans to add additional personnel in 2024 to watch self-checkouts, which will add to the cost of doing business.

Building products company Boral noted that input materials inflation surged over the past year, with higher transport, energy and labour costs. Despite these input cost increases, Boral increased profits by passing these on to customers, increasing the price of concrete and cement by 12 and 8 per cent, respectively.

Inflation is negative for consumers as it erodes their purchasing power, but it benefits those with existing assets with revenues linked to inflation. The best examples of companies with this characteristic are the toll road operators Transurban and Atlas Arteria, which saw strong increases in revenue from both inflation-linked tolls and higher traffic volumes. Their largest cost of interest repayments barely increased as these companies fixed their interest costs during periods of low-interest rates for a long duration.

Weaker Australian dollar

While the falling Australian dollar is a negative for Australians looking for a winter holiday in the south of France or Qantas buying jet fuel in US dollars on the world market, it is positive for Australian companies earning profits offshore. Over the past year, we have seen the Australian dollar trend downwards compared to most large currencies but most significantly against the USD. The weakening Australian dollar has provided a tailwind for companies that earn revenues in foreign currencies. Once earnings and dividends are translated into weaker Australian dollars, local investors enjoy elevated earnings per share and dividend per share growth. Some companies that benefitted from this tailwind in August were CSL, which saw dividends increase by +18%, and Amcor, where dividends rose by +13% once converted into Australian dollars.

Show me the money

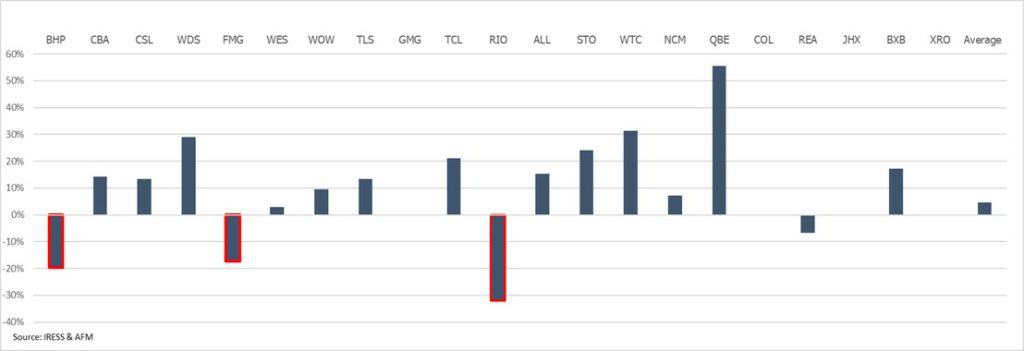

Unlike the previous few reporting seasons, August 2023 saw companies cut dividends, and share buy-backs were not a feature outside of Commonwealth Bank, Qantas and Computershare. Across the ASX Top 25 stocks (that reported - the other banks have a different financial year-end), the weighted average increase in dividends was 4%. The three miners, BHP, RIO and Fortescue, cut their dividends on weaker profits, higher costs and an uncertain outlook, with Xero not paying a dividend and James Hardie replacing their dividend with a buy-back. On the positive side of the ledger, QBE, Transurban and Woodside offset the cuts, posting strong increases in cash flows to their shareholders.

Figure 1: Dividend growth per share – ASX Top 25 August 2023

Best and worst

Over the month, Altium Limited, Inghams Group, GUD Holdings, Johns Lyng Group, Life 360 and Wesfarmers delivered the best results over the month. Despite the uncertain economic environment, especially around higher interest rates, these companies were able to combat these costs by lowering their gearing and leverage ratios whilst still being able to grow the business, in some cases lower losses, along with optimistic outlooks for 2024.

Looking at the negative side of the ledger, Chalice Mining, Core Lithium, Alumina Limited, Fletcher Building, Costa Group Holdings reported poorly received results by the markets. The common themes amongst this group are a delay or cancellation of dividends due to a potential takeover (Costa Group) or due to a lower earnings environment (Alumina) combined with lower profit guidance moving forward. Additionally, high price-to-earnings (PE) companies such ResMed, WiseTech and Ramsay that delivered profits below expectations or gave weak guidance saw their share prices sell off.

Result of the season

Before the August 2023 reporting season, conglomerate Wesfarmers would not have been many investors pick (including ours despite holding it in our portfolio) for the result of the season. Many in the market expected Wesfarmers’ earnings to contract based on a weaker domestic consumer, however the company grew profits on a strong rebound in Kmart, as well as growth in Bunnings, Officeworks and chemicals. Record Kmart earnings indicates consumers switching to the company’s low-price offer. Additionally, management provided upbeat guidance for 2024 which will see the first earnings from the Mt Holland lithium mine with the share price rallying by +11% in August.

Our Take:

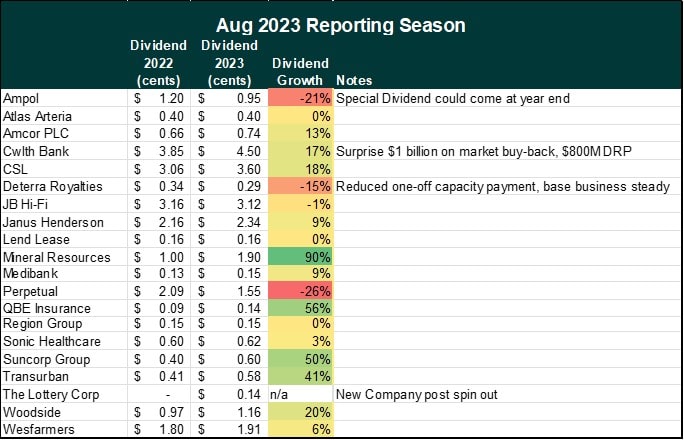

Overall, we were reasonably pleased with the results from the reporting season with most of our portfolio companies able to increase earnings and dividends with some reporting record profits in a tougher economic environment.

Figure 2: How did the portfolio fare?

As a long-term investor focused on delivering income to investors, we look closely at the dividends paid out by the companies that we own and whether they are growing. After every reporting season, we look to "weigh" the dividends that our investors will receive. Our view is that talk and guidance from management are often cheap, and that company CFOs can use accounting tricks to manipulate earnings, but actually paying out higher dividends is a far better indicator that a business is performing well. Additionally, global macroeconomic events and market emotions can temporarily cause the share prices of companies performing well to fall.

Using a weighted average across the portfolio, our investors' dividends will be +15% greater than for the previous period in 2022, and every company held in the portfolio was both profitable and paid a dividend.

On this measure, we are pleased with the results of the August 2023 reporting season.

Yours faithfully,

Allied Wealth Investment Committee

What sets Allied Wealth apart

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

General advice warning

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not take into account your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160

When you’re trying to navigate your finances and unlock a future of financial freedom, choosing an independent financial advisor that has your back and your best interests in mind is crucial.

Just one quick Google search will unlock a number of different independent financial advisors, but which one will be best for you?

Choosing an independent financial advisor that aligns with your goals and has ample experience in the Australian financial landscape is crucial, at Allied Wealth we have the tools to help you on your financial journey. These are our six key considerations we think you should keep in mind when you are trying to choose an independent financial advisor.

Independent financial advisors are a great choice when you’re looking for an independent financial advisor. Independent advisors like our team at Allied Wealth aren’t tied to a specific financial institution so you can be sure that the advice you receive is completely unbiased and based on your best interests. This independence also allows them to give you objective advice that is tailored to your unique financial situation.

Financial planning isn’t easy, and experience and expertise is crucial to ensure you get relevant advice. When you’re picking an independent financial advisor you may want to consider the number of years experience they have. At Allied Wealth our independent financial advisors have over 20 years of experience so you can be sure you’re getting informed, relevant and tailored advice.

Before you commit to a decision, you’ll want to check out what other people have to say about the services on offer. Checking out client reviews and testimonials is a great way to gauge how satisfied previous clients have been with the independent financial advisor you’re considering. At Allied Wealth, we value your satisfaction – and our client testimonials are proof of our commitment to offering quality advice.

A good independent financial advisor prioritises you and your individual goals and dreams. Pay attention to whether or not your independent financial advisor listens to your concerns and goals, and how well they tailor their advice to your specific financial situation. We are committed to maintaining a client-centric approach to fully understand your circumstances and how we can best help you reach your financial goals.

When choosing an independent financial advisor, understanding how they charge is crucial. You may want to ask for a breakdown of the fee’s to understand exactly how your independent financial advisor is being compensated. Fee transparency is a crucial aspect to build trust between you and your advisor.

You’ll want to look for an independent financial advisor who offers a comprehensive range of services that meet all your needs. Whether you’re after retirement planning, wealth management or wealth growth strategies, our team at Allied Wealth can help you out!

At Allied Wealth, we are committed to independence, experience and your overall satisfaction. If you’ve been on the hunt for an independent financial advisor but haven’t had any luck, contact us for all the tips and tricks you need to find an independent financial advisor who prioritises you with Allied Wealth.